What does the dot plot reveal?

In the morning of September 21st, the FOMC meeting came to a close.

Not surprisingly, the Fed raised rates again this month by 75bp, largely in line with market expectations.

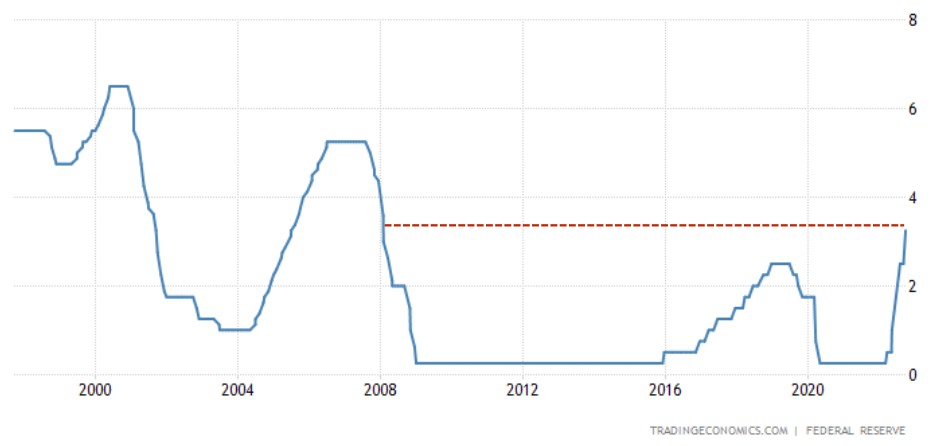

This was the third significant 75bp rate hike this year, taking the Fed funds rate to 3% to 3.25%, its highest level since 2008.

Image source: https://tradingeconomics.com/united-states/interest-rate

As the market had generally assumed before the meeting that the Fed would also raise rates by 75 basis points this month, the market's main focus was on the dot plot and economic outlook published after the meeting.

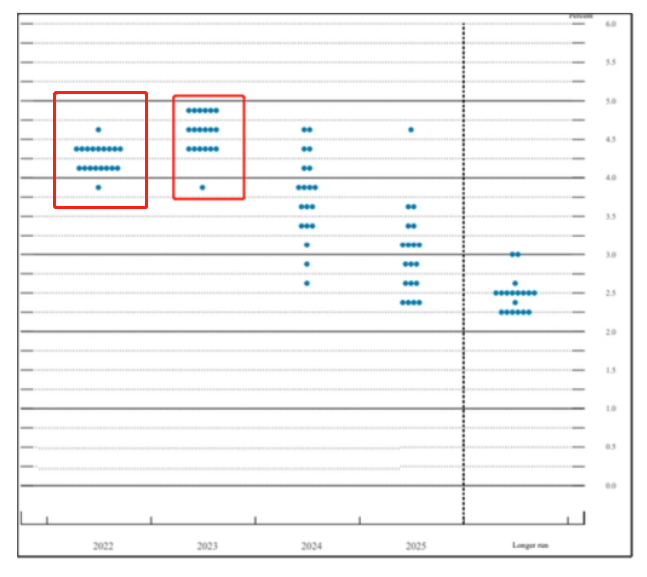

The dot plot, a visual representation of all Fed policymakers' interest rate expectations for the next few years, is presented in a chart; the horizontal coordinate of this chart is the year, the vertical coordinate is the interest rate, and each dot in the chart represents a policymaker's expectation.

Image source: the Federal Reserve

As shown in the chart, the vast majority (17) of the 19 Fed policymakers believe interest rates will be 4.00%-4.5% after two rate hikes this year.

So there are currently two scenarios for the two remaining rate hikes before the end of the year.

1. 100 bps rate hike by the end of the year, two hikes of 50 bps each (8 policymakers are in favour).

2. Two meetings remain to raise rates by 125 bps, 75 bps in November and 50 bps in December (9 policymakers are in favour).

Looking again at the expected rate hikes in 2023, the vast majority of votes are evenly split between 4.25% and 5%.

This means that the median interest rate expectation for next year is 4.5% to 4.75%. If interest rates are raised to 4.25% at the remaining two meetings this year, this means that there will only be a 25 basis point rate hike next year.

So, according to the expectations of this dot plot, there won't be much room for the Fed to raise rates next year.

And as for interest rate expectations for 2024, it is clear that policymakers' opinions are very far apart and do not have much relevance for the present.

What is certain, however, is that the Fed's tightening cycle will continue - with stronger rate hikes.

The tougher you are now, the shorter the crunch

Wall Street believes the Fed's goal is to create a "tougher, shorter" tightening cycle that will eventually slow economic growth in return for cooling inflation.

The Fed's outlook for the future of the economy, announced at this meeting, supports this interpretation.

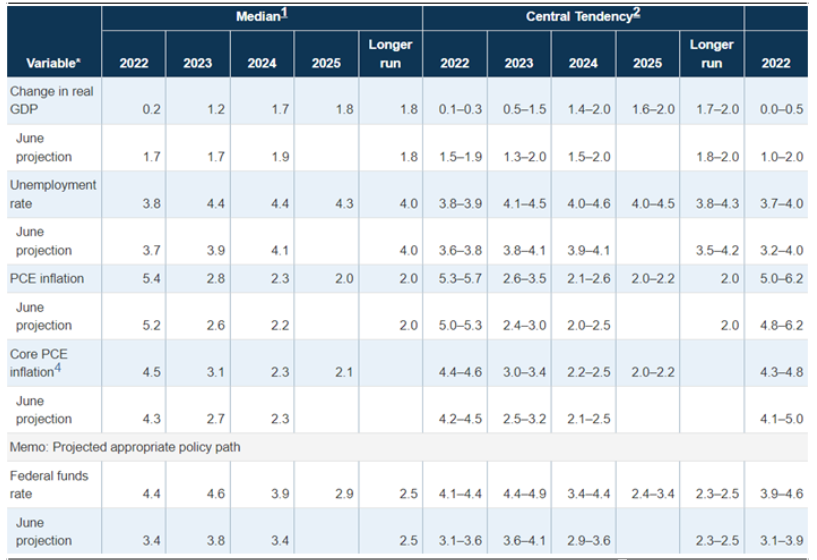

In its economic outlook, the Fed revised its forecast for real GDP in 2022 sharply downward to 0.2% from 1.7% in June, and also revised upward its forecast for the annual unemployment rate.

Image source: the Federal Reserve

This shows that the Federal Reserve has begun to worry that the economy may be entering a recession cycle, as economic and employment forecasts are increasingly pessimistic.

At the same time, Powell also bluntly said at the post-meeting press conference, " As aggressive rate hikes proceed, the chances of a soft landing are likely to diminish.

The Fed also acknowledges that further aggressive rate hikes are very likely to lead to recession and blood in the markets.

In this way, however, the Fed can complete the task of "fighting inflation" ahead of time, and the rate hike cycle will end.

Overall, the current rate hike cycle is likely to be a "hard and fast" action.

Interest Rate hike could be completed ahead of schedule

Since this year, the cumulative rate hike by the Fed has reached 300bp, combined with the dot plot to see the rate hike process will continue for some time, the policy stance in the short term and will not change.

This completely dispelled the market's thoughts that the Fed would quickly move to ease, and as of now, the yield of ten-year U.S. bonds has shot all the way up, and is about to reach the high of 3.7%.

But on the other hand, the Federal Reserve in the economic forecast for recessionary concerns, as well as the dot plot for the pace of interest rate increases next year is expected to slow down, which means that the process of raising interest rates, although still underway, but the dawn has appeared.

In addition, there is a lag effect in the Fed's rate hike policy, which has not yet been fully digested by the economy, and while the next rate hikes will be more reckless, the good news is that they may be completed sooner.

For the mortgage market, there is no doubt that interest rates will remain high in the short term, but perhaps the tide will change next year.