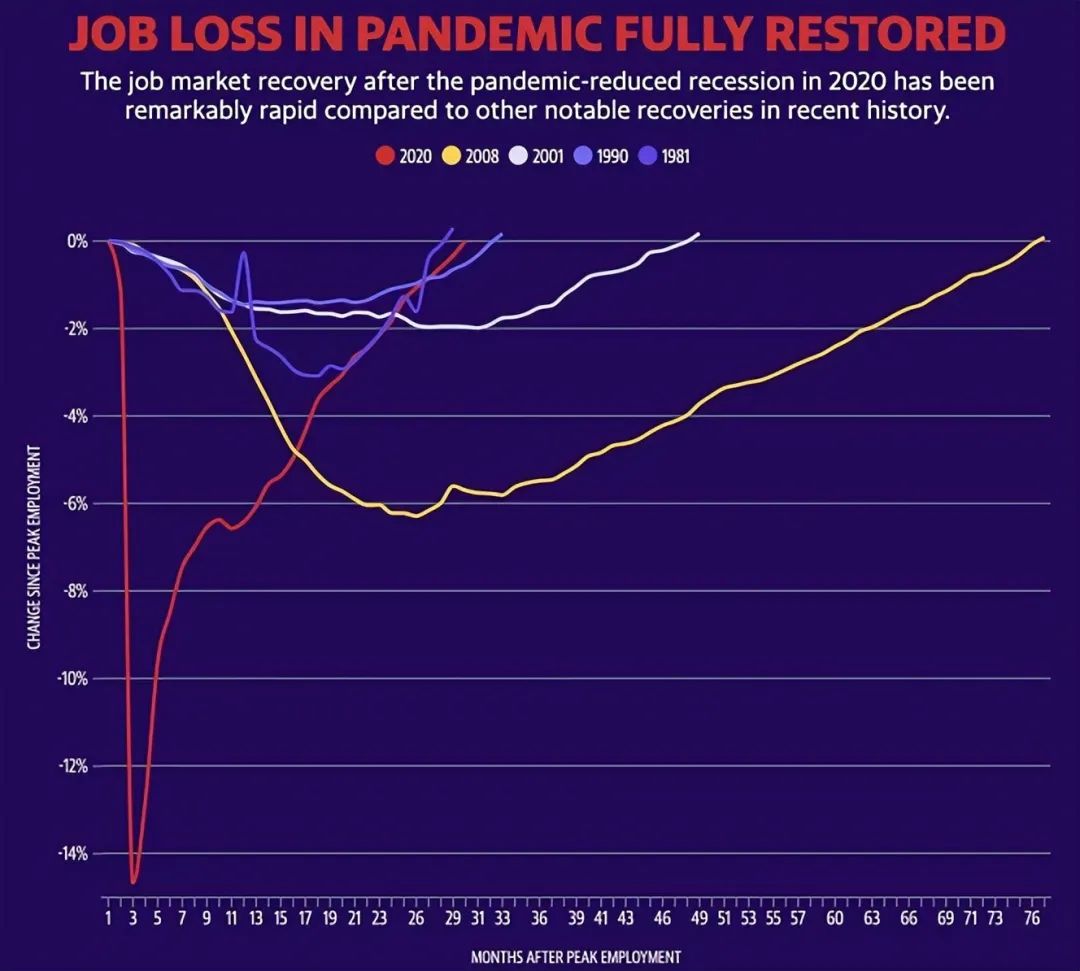

The latest data from the Labor Department showed non-farm employment increased by 528,000 in July, which is sharply better than the market expectations of 250,000. And the unemployment rate fell to 3.5%, returning to pre-pandemic levels in February 2020.

Source from CNBC

Seems to be a good standing data actually was a blow to the market, which had lost its fight with the Federal Reserve.

What did the Market do to resist?

Since last year, the Fed has miscalculated twice in a row, first by underestimating the persistence of inflation and then by overestimating its ability to tamp it down with higher interest rates.

At the end of last year, Powell was still stressing that the high inflation was temporary.

Markets are increasingly considering that the Fed may be making a third mistake -- relying too heavily on employment as a gauge of the economy and underestimating the timing of a recession.

Before last Thursday (August 4th, 2022), six Fed officials had delivered the ŌĆ£HawkishŌĆØ speeches on various occasions, sending a clearing message to markets that ŌĆ£do not underestimate the power of FedŌĆÖs fight with inflationŌĆØ.

The series of unified speeches are intended to warn the markets to stop being naysayers with the Fed.

The interesting thing is that the markets have been quite unmoved by the speeches and are beginning to bet that the Fed will ŌĆ£Give inŌĆØ soon in the face of recession risks and turn on the tightening path, while forecasting there will be a slower rate rise as soon as the September meeting.

The situation seems turning to ŌĆ£the Fed doesnŌĆÖt willing to against the marketsŌĆØ from ŌĆ£donŌĆÖt fight the FedŌĆØ gradually.

Under the guidance of this expectation, the stocks began to rise and the bond yield began to plummet. The markets are acting out of line with the FedŌĆÖs message, and in a sense they are against the Fed - the final judge will be the economic data.

The Fed wins.

Regardless of whichever data elements the market starts to return to reality with July non-farm data released.

Source from online

On top of that, the number of jobs added in May and June was revised 28,000 higher than previously reported, suggesting that the demand of labor remains strong and significantly easing fears of a recession.

Overall, the hot labor market has cleared the way for the Fed to maintain its aggressive rate hike path.

After the Fed had sent its strongest tightening signal in decades, the market went about its business as usual, even helping the stock market to show their best performance in recent years.

To markets unexpectedly, while it began betting on a shift in Fed policy, pushing stocks higher and Treasury yields lower, more demand was spurred, easing the risk of a recession and offsetting the FedŌĆÖs efforts to control inflation at the same time.

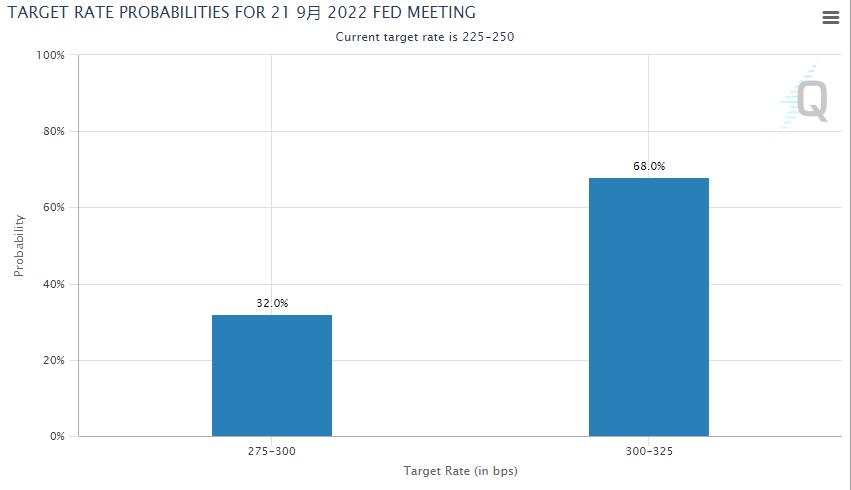

Following the report released, the probability of a 75 bp rate hike at the FedŌĆÖs September meeting soared to 68%, far higher than the probability of a 50 bp rate hike as predicted. (CME FedWatch Tool)

The non-farm data did chill the over-optimistic market -- expectations of more rate rises soared in a dramatic turn that reaffirmed the Wall Street mantra never ever try to against the Fed.

Who Misguided the Markets?

As weŌĆÖve mentioned in the previous articles, the Fed policy has been searching for a balance between ŌĆ£inflationŌĆØ and ŌĆ£unemployment rateŌĆØ.

It is obvious that the Fed has chosen ŌĆ£controlling inflation riskŌĆØ over ŌĆ£sacrificing the economyŌĆØ. The result will be to sacrifice the economy, albeit to a different extent.

What we need to know is that the Fed will have to move fast on the tightening path before inflation gets back to where it ideal position is.

The Fed may be on the verge of raising interest rates by 75 bp in September. Now letŌĆÖs expect the following performance of CPI.