Further slowing of the pace!

Last Wednesday, the February meeting of the FOMC came to an end.

As widely expected by the market, the Federal Reserve's Monetary Policy Committee announced a 25 basis point rate hike, raising the target range for the federal funds rate from 4.25%-4.50% to 4.50%-4.75%.

This is the second consecutive slowdown in the FedŌĆÖs rate hike pace and the first rate hike of only 25 basis points since March of last year.

Following the news, U.S. bond yields fell sharply to a new two-week low of 3.398%, down from 3.527% the previous day.

The market believes that the Fed is on track to slow down rate hikes and that a pause this spring has become more likely.

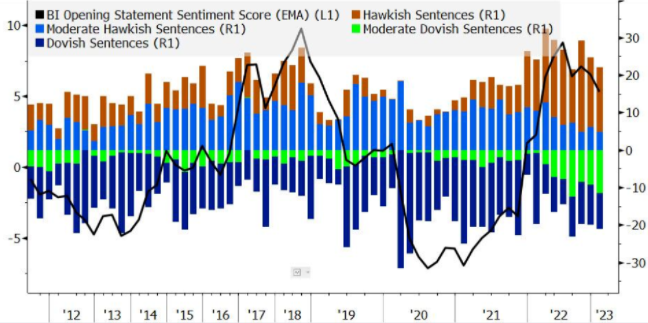

The biggest difference from the previous meeting is that, for the first time, there is recognition that inflation has moderated to some degree.

(Image Source: Bloomberg)

This means that the inflation indicators closely watched by the Fed are moving in a favorable direction - which basically confirms that the FedŌĆÖs interest rate hike process is at its end.

The penultimate X rate hike?

Compared to the statement made at the rate meeting, Fed Chairman Jerome PowellŌĆÖs post-meeting press conference is often more noteworthy.

At that press conference, reporters frantically probed PowellŌĆÖs questions about when he will stop raising rates.

In the end, Powell did not withstand the pressure, halfway or ŌĆ£leakedŌĆØ so the market tended to confirm the end of rate hikes soon!

Powell said the FOMC is discussing raising rates a few more times (a couple more) to restrictive levels, then pausing; and he said policymakers do not believe itŌĆÖs time to pause rate hikes.

Most market participants interpreted this statement (a couple more) as two more rate hikes.

This means that interest rates will continue to be raised by 25 basis points in March and May, which implies an increase in the policy rate to a range of 5% to 5.25%, in line with expectations for maximum interest rates as shown in the December dot plot.

However, despite Powell's hint of two more rate hikes, the market expects only one more in March.

Currently, the expectation of a 25 basis point rate hike in March is 85%, and the market believes that the prospect of another Fed rate hike in May has diminished.

The market no longer cares about the Fed

There has been a fierce battle between the market and the Fed since last November, but now the balance between the market and the Fed seems to be tipping in favor of the former.

The last three months have seen a significant loosening of financial conditions: Stock markets rose, bond yields fell, mortgage rates fell from their highs, and in January of this year, U.S. stocks actually posted their best performance since 2001.

From the market's performance, the last two rate hikes, the market almost all digested the results of the rate hike down to 50bp and 25bp in advance.

There is a clear sense that the market is much less worried about the Fed compared to the period before December 2022 - the market no longer seems to care about the Fed.

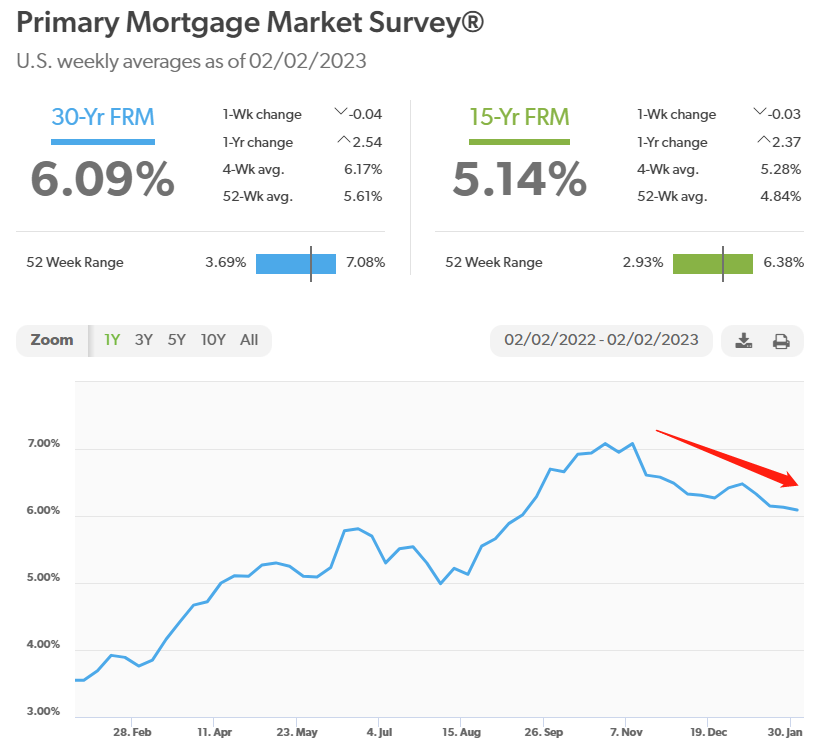

While the Fed continues to raise short-term rates, intermediate and long-term rates, which are largely influenced by investor expectations (such as most mortgage rates), have stopped rising or have begun to gradually decline.

õĖ©30-year mortgage rates have gradually fallen from their peak in October (Image Source: Freddie Mac)

In addition, even stronger-than-expected employment and economic growth data did nothing to change the marketŌĆÖs inclination.

The market generally believes that the current level of interest rates has risen to a level that could lead to a recession and that the Federal Reserve may begin cutting rates this year.

And with that impact, the downward trend in mortgage rates becomes more pronounced.